Introduction

Credit card interest rates closely follow Federal Reserve policy. As benchmark rates shift, credit card APRs often adjust quickly.

What does this mean for consumers carrying balances?

Why Credit Card APRs Are So Sensitive

Unlike fixed-rate loans, most credit cards have variable rates tied to:

- The prime rate

- Federal funds rate movements

This means changes can appear within billing cycles.

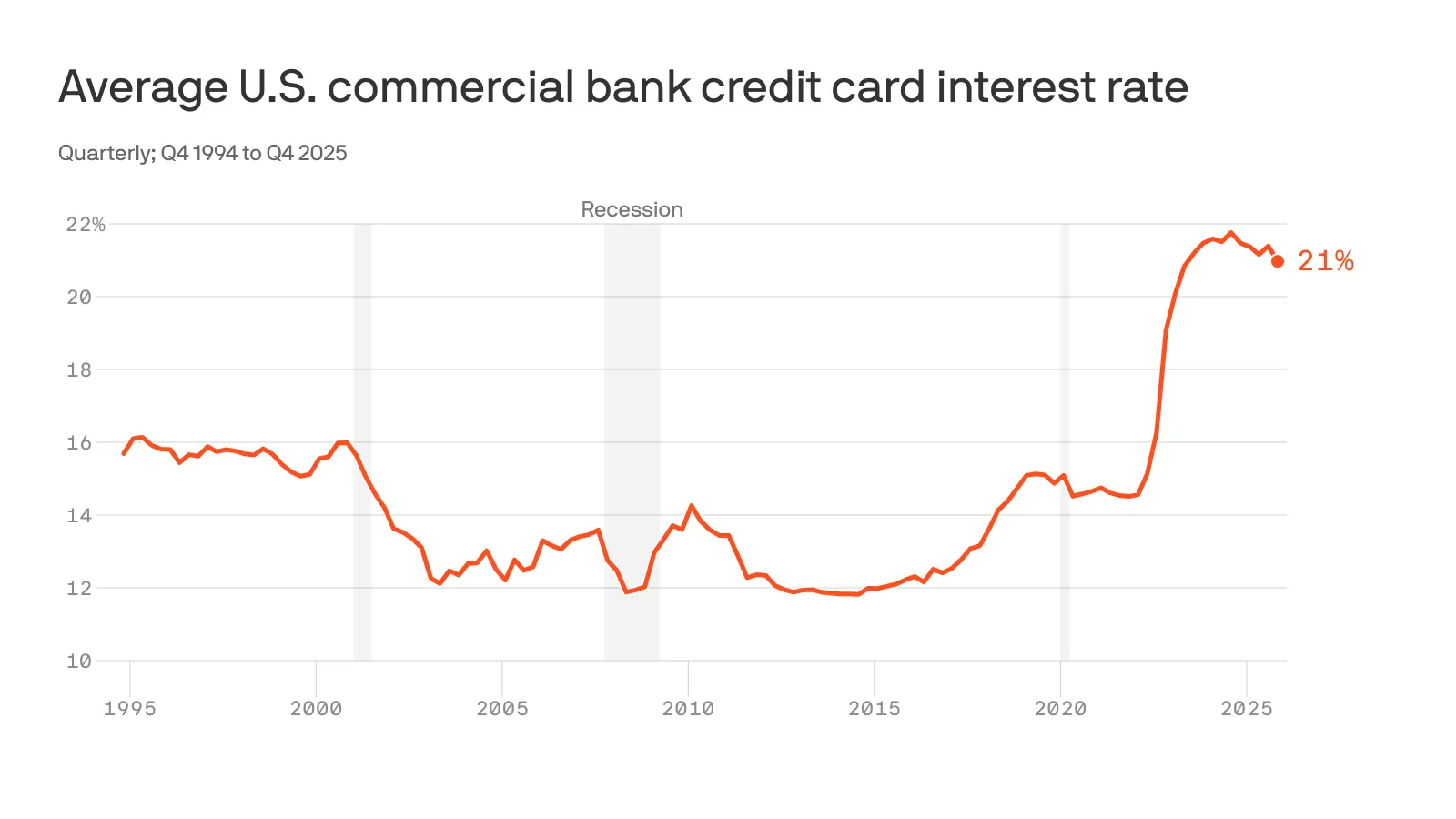

Average APR Trends

Recent trends show:

- Average APRs near historic highs

- Higher costs for new cardholders

- Promotional offers becoming more selective

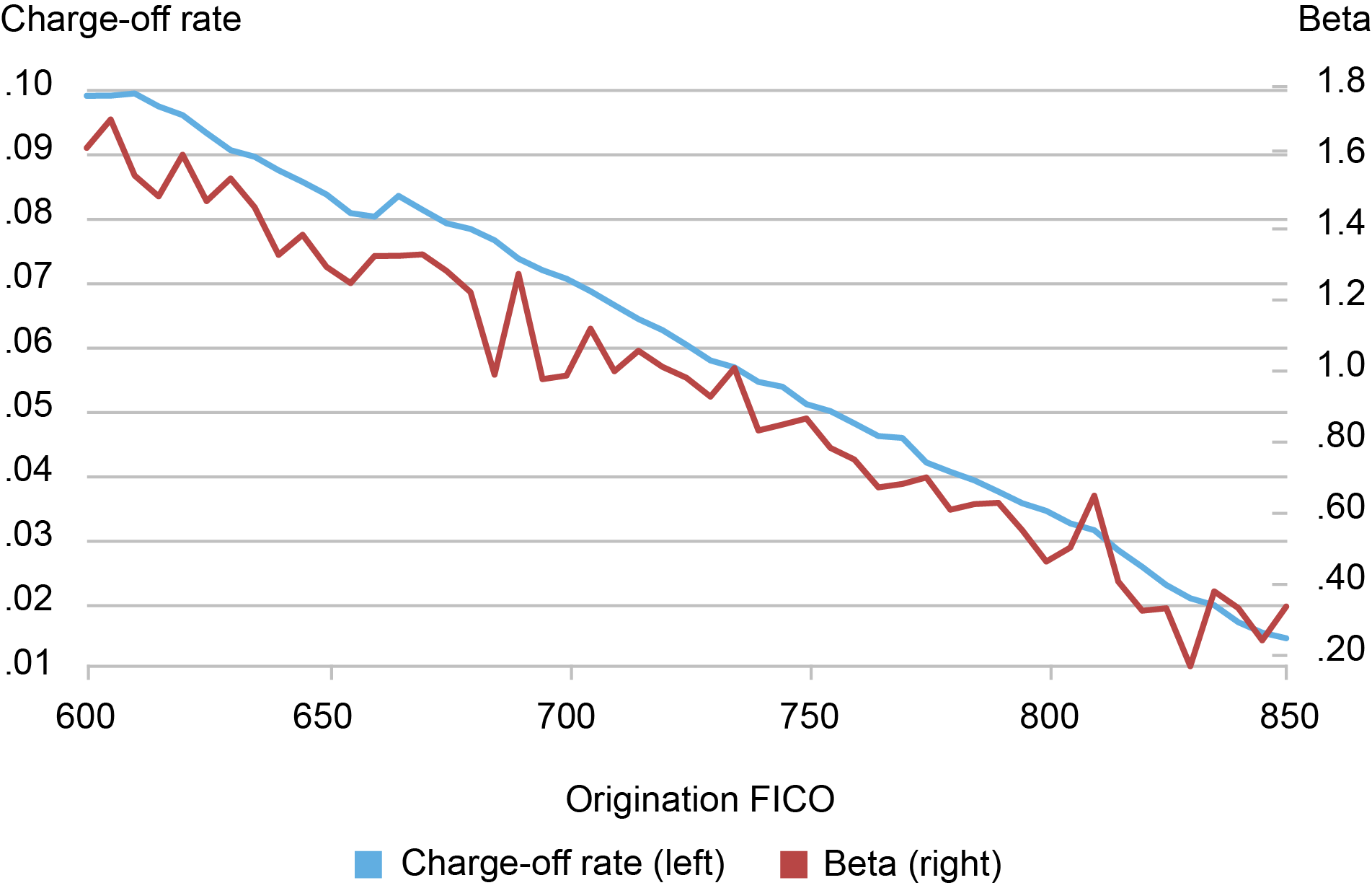

Consumers with lower credit scores often face the highest rates.

The Cost of Carrying a Balance

Example:

A $5,000 balance at a high APR can accumulate significant interest annually.

Even minimum payments may primarily cover interest rather than principal.

Strategies to Reduce Interest Burden

Consumers may consider:

- Balance transfers

- Negotiating lower rates

- Debt consolidation loans

- Paying more than the minimum

Improving credit scores can also unlock better offers.

Impact on Consumer Spending

Higher borrowing costs may:

- Reduce discretionary spending

- Slow retail growth

- Increase savings behavior

Credit conditions play a major role in overall economic activity.

Final Thoughts

As interest rates remain elevated, managing credit card debt becomes increasingly important. Awareness and proactive financial planning can reduce long-term borrowing costs.