Introduction

The Federal Reserve’s latest interest rate decision has once again drawn national attention. While headlines often focus on Wall Street’s reaction, the real impact is felt much closer to home — in household budgets, mortgage payments, credit cards, and savings accounts.

So what does this rate decision actually mean for American families in 2026?

Let’s break it down in practical terms.

What Happened?

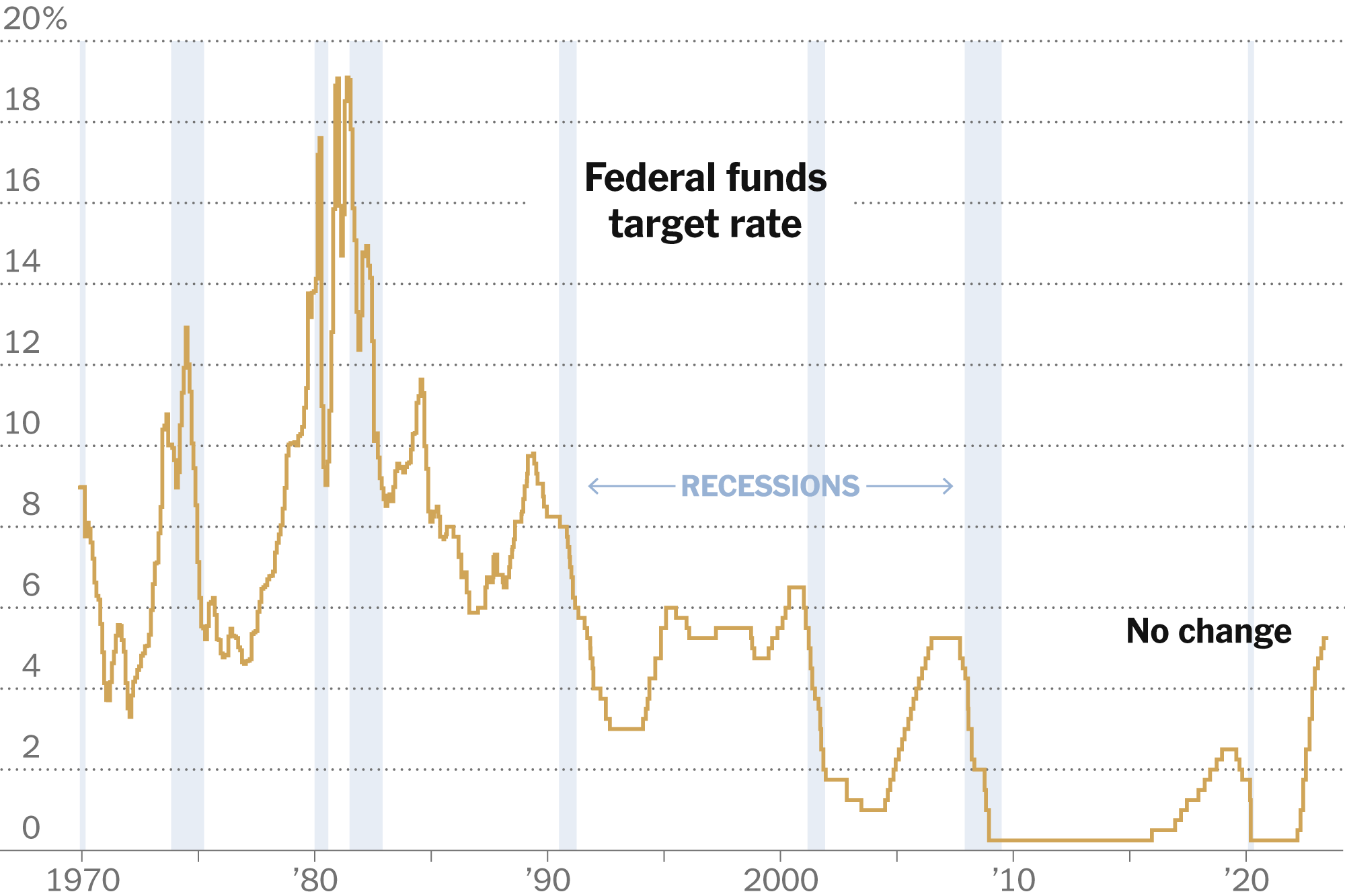

In its most recent meeting, the Federal Reserve announced that it would maintain/adjust the federal funds rate in response to ongoing inflation trends and labor market data.

The federal funds rate influences:

- Mortgage rates

- Credit card APRs

- Auto loans

- Personal loans

- Savings account yields

Even small adjustments can significantly affect borrowing and saving costs across the economy.

Why the Fed Adjusts Interest Rates

The Federal Reserve has a dual mandate:

- Maintain price stability (control inflation)

- Promote maximum employment

When inflation rises too quickly, the Fed increases interest rates to:

- Slow consumer spending

- Reduce business borrowing

- Stabilize prices

When the economy weakens, it lowers rates to encourage growth.

How This Impacts Mortgage Payments

Higher interest rates directly affect homebuyers.

Example:

A 1% increase in mortgage rates on a $350,000 loan can raise monthly payments by hundreds of dollars.

This means:

- Fewer people qualify for home loans

- Housing demand may cool

- Home prices may stabilize

For existing homeowners with fixed-rate mortgages, the impact is minimal. However, adjustable-rate mortgage (ARM) holders may see payment increases.

Credit Card and Consumer Debt

Credit card APRs are highly sensitive to Fed rate changes.

When rates rise:

- Credit card interest increases

- Carrying a balance becomes more expensive

- Minimum payments may increase

For households already managing debt, this can tighten monthly budgets.

Tip for consumers:

Consider paying down high-interest debt first during high-rate environments.

Impact on Savings Accounts and CDs

The good news?

Higher rates often mean:

- Better savings account yields

- Higher CD returns

- Improved money market rates

For savers, this can be an opportunity to earn more on idle cash.

What This Means for Everyday Spending

When borrowing becomes more expensive:

- Consumers spend less

- Big purchases decline

- Businesses may slow hiring

This is how rate policy gradually cools inflation.

Who Is Most Affected?

Most affected groups include:

- First-time homebuyers

- Families carrying credit card debt

- Small business owners

- Variable-rate loan holders

Less affected:

- Fixed-rate mortgage holders

- Debt-free households

- High-cash savers

What Could Happen Next?

Future rate decisions will depend on:

- Inflation data

- Jobs reports

- Wage growth

- Consumer spending

If inflation slows, the Fed may pause or cut rates. If inflation persists, further tightening may occur.

Final Thoughts

Interest rate decisions may seem technical, but they shape everyday financial life.

Understanding how these changes impact mortgages, debt, and savings allows families to make smarter financial decisions — especially during uncertain economic periods.